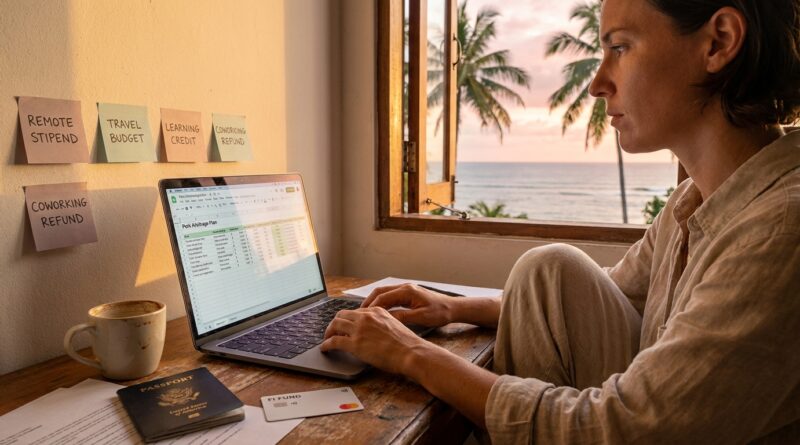

The New ‘Remote Stipend Arbitrage’: How To Turn Employer Perks Into A Nomad FI Accelerator

Rent is up. Flights are pricier. Coworking passes are not getting cheaper either. So it stings when you realize your employer may already be offering money that could cover part of those costs, and you have not claimed it. That is the quiet problem with remote work benefits. They often sit in a handbook, a buried HR page, or an onboarding PDF nobody reads twice. If you are trying to figure out how to use remote work benefits to reach financial independence as a digital nomad, this is one of the simplest places to start. You do not need a side hustle. You do not need to job hop. You need a system. The basic idea is simple. Turn every approved perk into either a cost you no longer pay yourself or cash you can redirect into index funds, your emergency fund, or extra runway for slow travel.

⚡ In a Hurry? Key Takeaways

- Remote stipends, education budgets, travel allowances, and wellness perks can directly cut your nomad costs and speed up your FI timeline.

- Start with a benefit audit, match each perk to a real expense, then automatically invest the money you no longer need to spend.

- Stay within company policy and tax rules. The goal is smart use, not gaming the system or risking reimbursement problems.

What “remote stipend arbitrage” actually means

It sounds fancier than it is.

Here, “arbitrage” just means using employer-paid benefits in a way that creates the most personal value for you. If your company gives you a $1,200 annual home office stipend and you already own a decent monitor, that benefit might help pay for a lightweight laptop setup, a portable hotspot, or noise-canceling headphones that support life on the road.

If the same company offers a learning budget, you might use it for a course that helps you move into a higher-paid role later. If they cover coworking, that can replace cafe spending, improve your productivity, and stop you from paying out of pocket for workspace in expensive cities.

The point is not to waste money on random “free” stuff. The point is to use approved perks to reduce your living costs and protect your investing rate.

Why this matters more in 2026

Many companies are doing a quiet tradeoff. They are getting stingier on base pay growth, and some are still adjusting salaries by location. At the same time, they are increasing flexible benefits because those perks are easier to offer than permanent salary raises.

That means two remote workers with the same job title can have very different financial outcomes. One takes the salary and ignores the extras. The other uses every approved benefit, cuts monthly spending, and keeps investing through rising costs.

Over a year or two, that gap gets big.

Step 1. Do a proper benefit audit

Most people guess what benefits they have. Do not guess.

Where to look

Check these places:

- Your offer letter

- Employee handbook

- HR portal or benefits dashboard

- Expense policy documents

- Learning and development pages

- Manager-approved team budget notes

What to search for

Look for words like:

- Work from home stipend

- Home office reimbursement

- Coworking reimbursement

- Internet or mobile subsidy

- Travel budget

- Offsite budget

- Education allowance

- Wellness stipend

- Equipment refresh cycle

- Phone reimbursement

- Relocation support

Make a simple spreadsheet

Create five columns:

- Benefit name

- Annual amount

- What it covers

- Claim deadline

- Best nomad use

This one small step is where hidden money usually shows up.

Step 2. Sort perks into three buckets

Bucket 1. Benefits that replace spending you already do

These are the easiest wins.

Examples:

- Internet reimbursement

- Phone plan support

- Coworking access

- Travel insurance tied to business travel

- Equipment stipends for laptop stands, keyboards, headsets, and monitors

If you would have paid for it anyway, this is almost like a raise.

Bucket 2. Benefits that improve your earning power

These do not always save money this month, but they can improve your FI math later.

Examples:

- Certifications

- Language classes

- Project management training

- AI tool subscriptions if approved

- Conference tickets

If a $1,500 education budget helps you qualify for a better role, that matters more than a free ergonomic chair.

Bucket 3. Benefits that improve your nomad logistics

This is where mobile workers often miss opportunities.

Examples:

- Team meetup travel paid by the company, which can reduce your own repositioning costs

- Temporary accommodation during offsites

- Relocation assistance

- Visa or immigration support for specific work arrangements

If you are already moving around, these benefits can shrink major one-time costs. That pairs nicely with strategies in Get Paid To Move: How Digital Nomads Can Stack Relocation Grants And Tax Breaks To Reach FI Faster, especially if you are planning your next base with incentives in mind.

Step 3. Match each benefit to your actual nomad life

This is where people either save real money or buy nonsense they do not need.

Ask three questions for every perk:

- Would I pay for this myself if the company did not cover it?

- Will this still help me if I change countries every one to three months?

- Does this reduce stress, increase income, or cut recurring costs?

Good matches for digital nomads often include:

- Portable second monitor instead of a full desktop setup

- International hotspot or eSIM-compatible gear instead of office-only hardware

- Coworking memberships with multiple city locations

- Telehealth or mental health support that works abroad

- Online courses rather than in-person local classes

The test is simple. Pick the version that travels well and continues saving you money.

Step 4. Ask for nomad-compatible substitutions

This is the part many workers skip because they assume the answer is no.

Sometimes the policy says “home office equipment,” but HR or your manager may approve functionally similar items that fit a remote lifestyle better.

Examples of reasonable asks

- Portable monitor instead of a fixed desktop screen

- Global coworking pass instead of one local office membership

- Roaming-friendly mobile plan support instead of standard office internet reimbursement

- Online certification instead of conference attendance

- Travel backpack or protective case if it clearly supports safe equipment transport and policy allows it

A script you can use

“I want to use the remote work benefit in a way that best supports my job while staying within policy. Since I work remotely across different locations, would it be possible to use the stipend for [item/service] instead of [standard option]? It serves the same work purpose and would help me stay productive while traveling.”

Short. Professional. Easy for HR to answer.

Step 5. Build your FI redirect system

This is the part that turns a nice perk into actual progress.

Every time a company benefit covers one of your normal expenses, redirect that exact amount somewhere useful. Do it automatically if you can.

Three smart destinations for the money

- Emergency fund, if your travel buffer is thin

- Low-cost index fund investments, if your safety net is already solid

- Travel sinking fund, if keeping mobility cheap helps you avoid debt

A simple example

Say your company covers:

- $100 per month coworking

- $60 per month internet and phone

- $1,000 annual learning budget

If you were going to pay that coworking and connectivity cost yourself, that is $160 per month freed up. Auto-invest that. The annual learning budget is different, but if it helps you earn more or avoid paying for training yourself, that still supports FI.

$160 a month invested consistently is not magic. But over years, it is real money. More importantly, it protects the habit of investing while your cost of living moves around.

Step 6. Watch the tax and policy fine print

This is the boring part. It is also important.

Not every stipend is tax-free. Not every reimbursement is available in every country. And not every purchase that feels work-related will qualify.

Check these details

- Does the benefit require receipts?

- Is it reimbursement only, or paid upfront?

- Does it expire each quarter or each year?

- Can it be used outside your home country?

- Does payroll treat it as taxable income?

- Will your manager need to pre-approve the purchase?

The cleanest approach is simple. Stay inside policy. Keep records. If anything feels fuzzy, ask before you spend.

Common perks remote workers forget to use

These are the ones that get missed a lot:

- Annual equipment refresh funds

- Backup internet reimbursement

- Ergonomic assessments that can justify approved gear

- Learning subscriptions and book budgets

- Wellness stipends that can cover apps, fitness memberships, or stress support

- Company-paid travel tied to meetups and retreats

- Professional association dues

Even small items matter. A $300 forgotten benefit is still $300 you do not have to earn, tax, and save from scratch.

What not to do

A few traps are worth avoiding.

Do not buy things just because the stipend exists

Free junk is still junk. If it does not reduce cost, improve work, or support your mobility, skip it.

Do not treat reimbursements like bonus spending money

If the perk replaces a normal expense, redirect the saved amount. Otherwise, the benefit disappears into random purchases and your FI date does not move.

Do not ignore expiration dates

Many budgets reset quietly. Put reminders in your calendar 60 days before they expire.

Do not assume HR knows the nomad angle

You may need to explain why a portable setup is the practical version of a home office setup. Be clear and polite.

A realistic monthly workflow

If you want this to stick, keep it simple.

Once per quarter

- Review all benefit balances and deadlines

- Check upcoming travel and work needs

- Submit any reimbursement claims you have been putting off

Once per month

- Total the expenses your company covered

- Transfer the same amount into savings or investments

- Track how much runway those perks created

That is how to use remote work benefits to reach financial independence as a digital nomad in real life. Not as a theory. As a routine.

At a Glance: Comparison

| Feature/Aspect | Details | Verdict |

|---|---|---|

| Work-from-home and equipment stipends | Best used for portable gear, connectivity tools, and items that replace out-of-pocket work costs. | High value if you choose travel-friendly essentials. |

| Education and training allowances | Can fund certifications, online courses, or tools that improve future earning power. | Strong long-term FI boost, even if savings are less visible today. |

| Travel, coworking, and relocation support | Helps cut some of the biggest nomad costs when policy allows flexible use. | Excellent for extending runway, but check rules and taxes carefully. |

Conclusion

There is a quiet advantage available to remote workers right now. Companies trying to compete for talent in 2026 are often adding benefits while keeping a tighter lid on salary growth and adjusting pay by location. That means the people who pay attention to perks are often the ones who keep moving, keep saving, and keep investing even when costs climb. Start with a benefit audit. Ask for nomad-friendly versions where it makes sense. Then redirect every dollar of saved spending toward your FI plan. It is a low-risk move, and it does not require a new job or longer hours. It just requires noticing the money that is already sitting there, waiting for you to use it well.